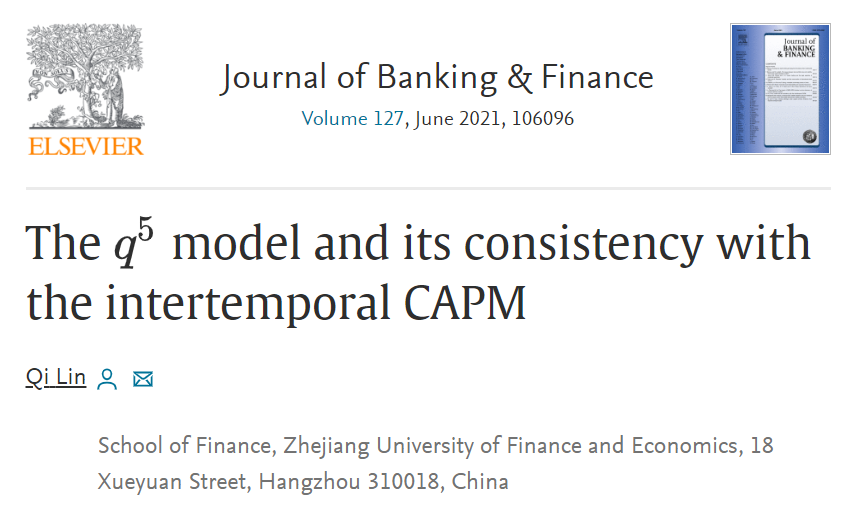

近日,公司林祺副教授以独立作者身份撰写的论文“The q5 model and its consistency with the intertemporal CAPM”在金融学国际权威学术期刊《Journal of Banking & Finance》上正式发表。

Abstract

In this paper, we test the consistency of the q5 model of Hou et al. (2019, 2020) with Merton’s (1973) intertemporal capital asset pricing model (ICAPM) framework. We find that all but one factors in the q5 model carry significantly positive covariance risk prices. The profitability factor, however, has little explanatory power for the cross-section of expected returns. The time-series tests show that the investment factor predicts a significant decline in stock market volatility, thereby being consistent with its positive price of covariance risk and satisfying the sign restrictions associated with the ICAPM. Importantly, the expected growth factor that is found to be helpful in describing cross-sectional average returns fails to predict future investment opportunities with the correct sign, which indicates that it is not a valid risk factor under the ICAPM. Overall, the ICAPM cannot be used as a theoretical background for the q5 model.

《Journal of Banking & Finance》由Elsevier出版,主要发表银行与金融等研究领域的理论与实证论文,收录于SSCI(Social Sciences Citation Index)。该期刊为国际学术界公认的金融领域高质量期刊,ABDC A*期刊,ABS 3星期刊。

澳门十大正规网站排行榜一直以来高度重视科学研究,将科研创新能力视为学科核心竞争力的重要组成部分,学院教师科研团队以一流团队建设标准严格要求,积极探索、勇于创新,积极参与国内国际合作,取得了一系列达到国际前沿水平的研究成果,为学校建设特色鲜明的一流财经大学贡献力量。